How West Virginia's Child Care Policy Compares to Neighboring States

Introduction

This is the third and final blog of this series.

A Recover Clarity policy analysis reviewed how West Virginia and neighboring states evaluate self-employed parents within child care assistance programs. The review focused on a practical question: should a parent be treated differently because their small business is structured as a single-member LLC rather than a sole proprietorship?

This question matters because many modern small businesses use LLCs. A single-member LLC may be a one-person business with modest income, irregular cash flow, limited assets, and ongoing need for child care. The LLC may exist for liability protection, business banking, insurance, customer credibility, contracting, or recordkeeping. It does not automatically mean the owner is wealthy or no longer needs support. And Small Businesses and Self-Sufficiency in Appalachia help both the communities, but play a role in recovery support as well, which is why Recover Clarity has taken up writing on this topic.

The analysis found that West Virginia’s current child care subsidy policy is more entity-structure focused than the neighboring states reviewed. Pennsylvania, Kentucky, Virginia, Maryland, and Ohio generally appear to evaluate self-employment through income, work activity, and documentation. West Virginia’s reviewed manual, by contrast, expressly excludes LLCs, C corporations, S corporations, and partnerships from self-employment approval under the policy section reviewed. This is all regardless of need for child care, income, or work performed.

The Central Policy Question

Verification Versus Entity Exclusion

No serious policy analysis should argue that self-employment should go unverified. It should be verified. Public programs need income rules, work requirements, documentation standards, and program-integrity protections. The question is how verification should occur.

A verification-based approach asks whether the parent is working, whether income is within program limits, whether documentation supports the work activity, and whether child care is needed. An entity-exclusion approach asks whether the parent’s business structure falls within an allowed category. Those two approaches can produce very different results, potentially hurting small business structures within a state and leaving people in true need of assistance or subsidies to make hard decisions about their work and lives.

Why LLC Ownership Matters

The IRS explains that, for federal income tax purposes, a single-member LLC is generally treated as disregarded as separate from its owner unless it elects corporate treatment (Internal Revenue Service, 2025). The SBA describes LLCs as a business structure that can provide personal liability protection in many instances (U.S. Small Business Administration, 2025).

That means a single-member LLC can function much like a sole proprietorship for income-reporting purposes while providing legal and business formalization benefits. If a child care policy treats one structure as acceptable and the other as disqualifying, the distinction may be based more on legal form than economic reality.

West Virginia's Current Framework

What the Reviewed Manual Says

West Virginia’s current Child Care Subsidy Policy and Procedures Manual distinguishes among forms of self-employment and business ownership. The reviewed manual states that self-employment type approvals are limited to contracted sole proprietorships and that applicants participating as a member of a C corporation, S corporation, LLC, or partnership are not eligible for West Virginia Child Care Subsidy (West Virginia Department of Human Services, 2024).

This is not simply a missing clarification. LLCs are expressly listed as excluded under the reviewed framework. That makes West Virginia materially different from the comparison states reviewed for this project.

Why This Deserves Review

A policy can be clear and still deserve review. A policy can be longstanding and still become misaligned with modern work patterns. Many small businesses today operate as LLCs for basic liability and business reasons. If child care eligibility discourages that structure, the policy may unintentionally discourage formalization of LLCs or even cause people to close their businesses or change business structures leaving themselves more financially vulnerable.

This does not mean every LLC owner should qualify. Income, work activity, household size, documentation, and need for care still matter. The question is whether LLC ownership alone should control eligibility when a parent is otherwise similarly situated to a sole proprietor.

Pennsylvania

LLC Ownership Confirmed as Self-Employment

Pennsylvania provides one of the strongest comparisons because agency clarification obtained during this project indicated that LLC ownership can be accepted as self-employment. The clarification indicated that business structure affects documentation requirements, not categorical eligibility (M. Frank, personal communication, 2026).

Pennsylvania’s public Child Care Works materials describe the program as subsidized child care for low-income families who need care while working or attending education or training (Pennsylvania Department of Human Services, n.d.). The agency clarification adds an important practical point: a parent operating through an LLC can still be evaluated as self-employed if documentation supports the work and income.

Why Pennsylvania Matters

Pennsylvania demonstrates that a neighboring state can require documentation without categorically excluding LLC owners. This is a stronger finding than simply saying no exclusion was identified. Based on the clarification obtained, Pennsylvania affirmatively supports LLC ownership as compatible with self-employment review.

Kentucky

Broad Self-Employment Verification

Kentucky also provides a strong comparison. Kentucky’s Child Care Assistance Program manual recognizes self-employment and identifies business records as the primary source of verification for established self-employment. It lists acceptable verification sources such as statements from an outside accountant, ledger books, records or receipts maintained by the applicant, recent IRS tax forms, and other forms of documentation (Kentucky Cabinet for Health and Family Services, 2026).

The Kentucky manual also addresses S-corporation income. It states that S-corporation wages in which taxes are withheld are entered as earned income and that S-corporation distributions are entered as self-employment earned income for program purposes (Kentucky Cabinet for Health and Family Services, 2026).

Kentucky's Importance as an Appalachian Comparison

Kentucky is especially important because it is an Appalachian comparison state. Its framework shows that formal business structures can be addressed through income and documentation rules rather than categorical exclusion. Agency clarification obtained during this project further indicated that LLCs and S corporations may be evaluated through income and hour requirements.

This suggests that a state can preserve program integrity while still recognizing formal business structures. Even structures which have multiple means of household revenue such as S-corporation and they know the required documentation to account for all household income.

Virginia

LLC Income May Be Considered Self-Employment

Virginia’s child care subsidy guidance provides another important comparison. The guidance states that Virginia counts net income from self-employment, farm, or non-farm activity. It also states that if an individual incorporates a business, wages or salary from the corporation are considered regular earned income rather than self-employment income. Then the guidance makes a key distinction: limited liability companies are not incorporated, so the income may be considered self-employment (Virginia Department of Education, 2023).

This language is significant. Virginia expressly distinguishes LLCs from incorporated businesses and allows LLC income to be considered as self-employment. That is much stronger than merely saying no LLC exclusion was found.

Verification Still Exists

Virginia still requires documentation. The guidance discusses proof of earnings, business expenses, tax returns, receipts, and averaging of self-employment income. The point is not that Virginia ignores program integrity. The point is that Virginia appears to address self-employment through documentation and income rules rather than excluding LLCs automatically.

Maryland

Self-Employment Attestation

Maryland’s Child Care Scholarship Program materials require families to meet eligibility requirements related to work, training, school, and income (Maryland State Department of Education, n.d.-a). Maryland also provides a self-employment attestation statement for Child Care Scholarship applicants. The form asks for information about self-employment activity, work schedule, hours worked, and income verification, and states that the information will be verified and used to determine eligibility (Maryland State Department of Education, n.d.-b).

What Maryland Shows

Maryland’s materials show a process for self-employed applicants. The reviewed materials did not identify a comparable LLC-based exclusion. Like other comparison states, Maryland appears to focus on verification of work activity and income rather than excluding applicants solely because of business entity structure.

Ohio

Verification-Based Materials Reviewed

Ohio materials reviewed for this project did not identify a comparable restriction based solely on LLC ownership. Ohio’s publicly funded child care materials and forms reviewed during the project focused on income, work activity, self-employment verification, and documentation. Some Ohio materials identify self-employment forms as part of the child care application process.

Ohio is included cautiously because the public materials reviewed did not provide the same explicit LLC language found in Virginia or the agency clarification obtained for Pennsylvania. Still, the materials reviewed did not identify a comparable categorical exclusion.

What the Comparison Shows

The Pattern Across Neighboring States

The neighboring states reviewed generally ask practical eligibility questions: Is the parent working? Is the parent income-eligible? Can the parent document the work activity? Is child care needed? Does the family meet all other program rules?

West Virginia’s reviewed framework adds a stronger entity-structure barrier by excluding LLCs and other formal business entities from self-employment approval. That is the key contrast.

Strongest Comparison Points

The strongest comparison points are Pennsylvania, Kentucky, and Virginia. Pennsylvania agency clarification confirmed LLC ownership can be accepted as self-employment. Kentucky’s manual and agency clarification support a broader verification-based approach that can address formal business structures, including S-corporation income treatment. Virginia guidance expressly states that LLCs are not incorporated and that LLC income may be considered self-employment.

Together, these comparisons make the case that a verification-based approach is possible.

Why This Matters for West Virginia

Labor-Force and Workforce Participation

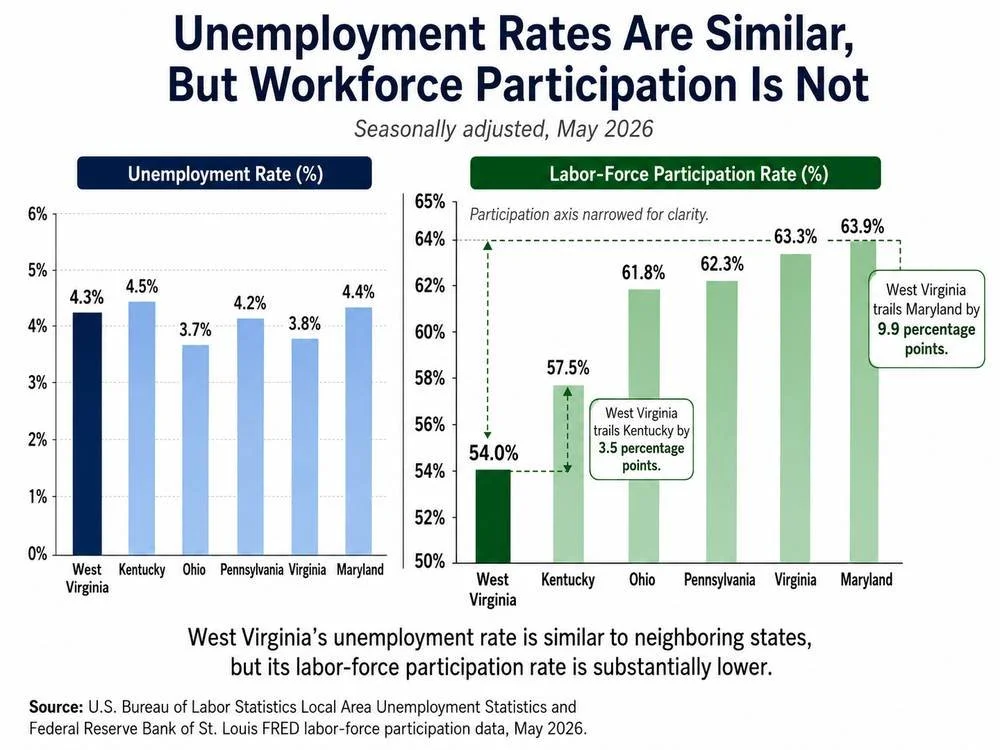

West Virginia’s labor-force participation rate remains among the lowest in the United States. Labor-force participation measures the share of a state’s civilian population that is either employed or unemployed but actively seeking work; it is broader than the unemployment rate because it captures how many adults are connected to the labor market at all (Federal Reserve Bank of St. Louis, 2026). As of May 2026, West Virginia’s seasonally adjusted labor-force participation rate was 54.0%, the lowest rate among the 50 states. By comparison, neighboring states had substantially higher participation rates: Pennsylvania was 62.3%, Ohio was 61.8%, Kentucky was 57.5%, Virginia was 63.3%, and Maryland was 63.9% (Federal Reserve Bank of St. Louis, 2026).

This comparison is important because West Virginia is already operating with a smaller share of its adult population attached to the workforce. When a state has a low labor-force participation rate, policies that affect whether parents can work, remain employed, maintain child care, or continue operating a small business deserve careful review. A policy that disrupts child care access may not only affect one parent’s household stability; it may also reduce workforce participation, limit self-employment, and weaken the ability of small businesses to continue operating.

Child care assistance functions both as a family-support policy and a workforce-support policy. The Child Care and Development Fund is the primary federal funding source for child care subsidies that help eligible low-income working families access child care (U.S. Department of Health and Human Services, 2025). Research supports the connection between child care assistance and continued labor-force participation. A U.S. Census Bureau analysis found that 98.3% of subsidy-receiving married mothers who worked during the study reference year remained in the labor force four years later, compared with 91.3% of similar working married mothers who did not receive a subsidy (Gurrentz, 2021).

The broader research literature also supports this relationship. Morrissey (2017) found that lower out-of-pocket child care costs and greater availability of early care and education are generally associated with increased maternal labor-force participation and work hours, although the size of the effect varies across studies. This means child care affordability and availability are not separate from workforce policy; they are directly connected to whether parents, especially mothers and low-income caregivers, can remain economically active (Morrissey, 2017).

In this context, a child care policy that discourages or disrupts lawful self-employment deserves careful review. For a parent operating a very small business, child care instability can affect the parent’s ability to work, the continuity of the business, the stability of any part-time employees, and the family’s ability to remain financially independent. In a state ranking last in labor-force participation, policy should be evaluated not only for technical eligibility compliance, but also for whether it supports or undermines workforce participation, entrepreneurship, and long-term economic stability.

Entrepreneurship and Business Formalization

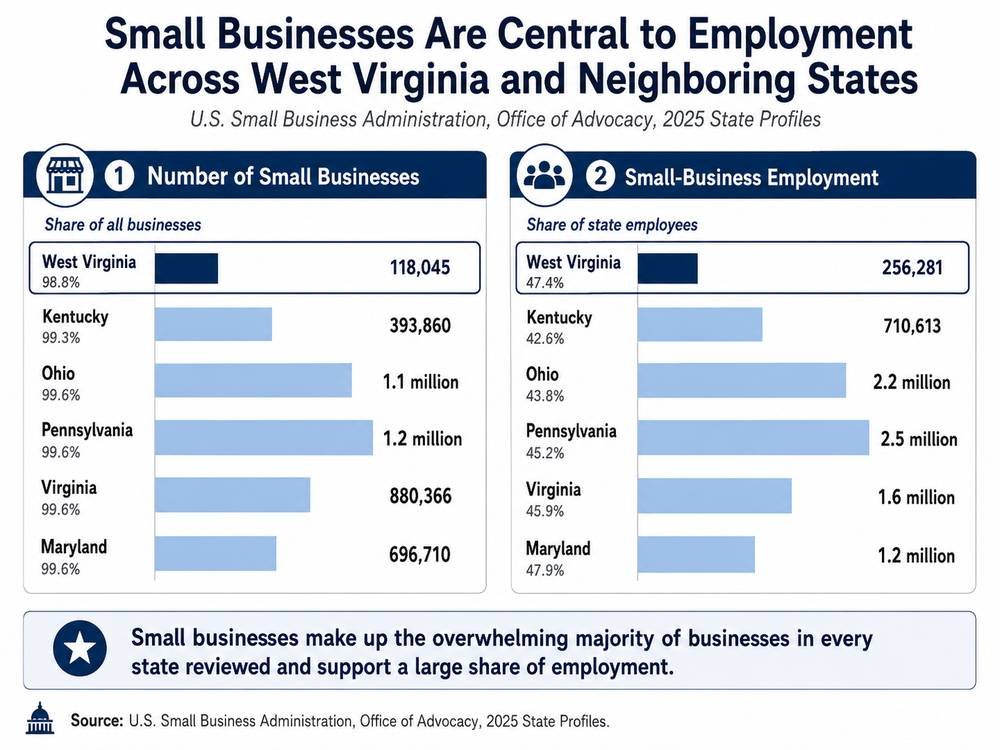

Small businesses make up the overwhelming majority of businesses in every state reviewed and support a large share of employment. In West Virginia, the SBA Office of Advocacy reports 118,045 small businesses, representing 98.8% of all businesses, and 256,281 small-business employees, representing 47.4% of state employment. This matters for child care policy because many working parents use formal business structures, including LLCs, for liability protection, banking, insurance, contracts, and credibility. A policy that discourages or excludes formal small-business structures may work against broader workforce and economic-development goals. Data source: U.S. Small Business Administration, Office of Advocacy, 2025 State Profiles.

West Virginia also has a clear interest in small-business development, entrepreneurship, and economic mobility. Business formalization is part of that process. When a parent forms an LLC, registers a business, opens a business bank account, files annual reports, obtains insurance, tracks income, or contracts with customers, that parent is often moving from informal work into more accountable, documented economic activity. That should generally be encouraged, not discouraged.

West Virginia’s own business registration system reflects this idea. The West Virginia One Stop Business Portal states that online business registration can complete registration with the West Virginia Secretary of State, the West Virginia State Tax Department, and WorkForce West Virginia, when applicable. In other words, formal registration can connect a business to tax, unemployment-compensation, and state-recordkeeping systems. Registered businesses are also required to file annual reports with the Secretary of State and pay the annual filing fee, which further supports public accountability and ongoing documentation.

This matters because West Virginia is already trying to grow and track business activity. In February 2026, the West Virginia Secretary of State reported 1,733 new business registrations for that month and 19,363 new businesses registered during the prior 12-month period, with 166,029 total businesses registered to do business in the state. Those figures show that business creation and formal registration are active parts of West Virginia’s economy.

Small businesses are also central to West Virginia’s employment base. The U.S. Small Business Administration Office of Advocacy reported that West Virginia had 118,045 small businesses in its 2025 state profile, representing 98.8% of all West Virginia businesses. Those small businesses employed 256,281 workers, or 47.4% of West Virginia employees. Nationally, the SBA reported 36.2 million small businesses, accounting for almost 46% of private-sector employment. This means West Virginia’s reliance on small-business employment is slightly higher than the national private-sector share reported by SBA.

Business formation data also shows that West Virginia participates in the same broader national trend toward new business activity. The U.S. Census Bureau’s Business Formation Statistics measure business initiation activity through applications for Employer Identification Numbers. In May 2026, West Virginia recorded 1,647 total business applications and 483 high-propensity business applications, meaning applications with characteristics associated with a higher likelihood of becoming businesses with payroll. Nationally, May 2026 business applications were 523,971, with 146,555 high-propensity applications.

For child care policy, the point is not that every LLC owner should automatically qualify for assistance. Income, household size, work activity, need for care, and documentation should still be verified. The concern is narrower: when a low-income parent has formed a legitimate small business entity for liability protection, banking, insurance, contracting, or credibility, the business structure itself should not end the eligibility review. A verification-based approach could allow West Virginia to protect program integrity while also supporting formal business records, tax compliance, legitimate self-employment, and long-term economic mobility. That balance is especially important in a state where small businesses make up nearly all businesses and employ nearly half of the workforce.

Family, Recovery, and Economic Stability

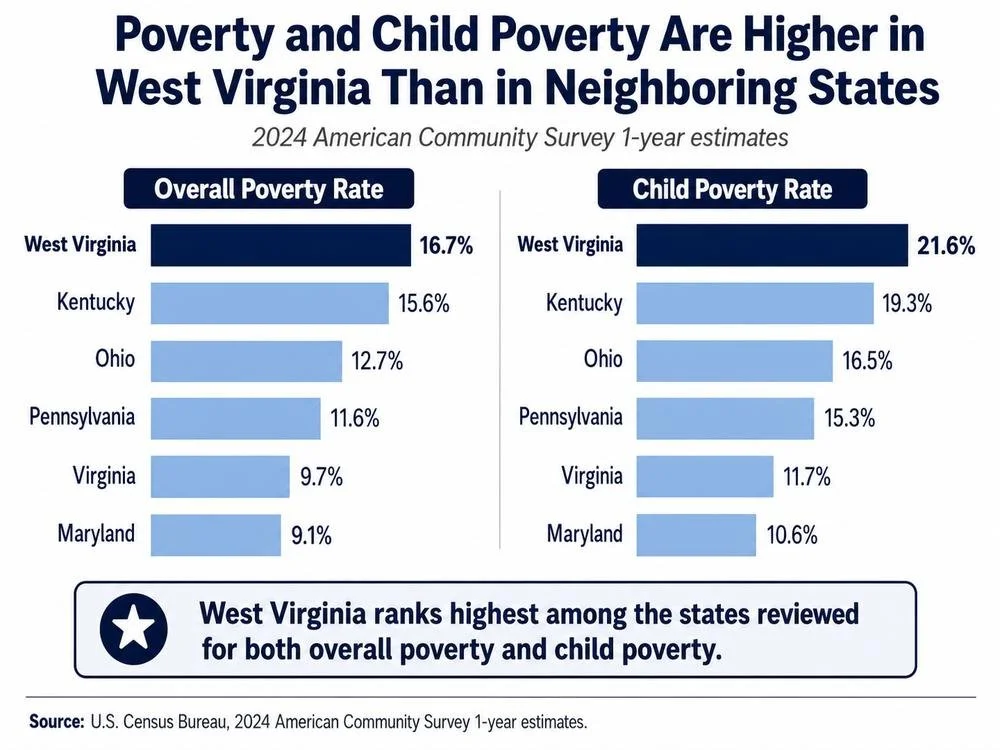

West Virginia ranks highest among the comparison states for both overall poverty and child poverty. The 2024 American Community Survey estimates show West Virginia’s overall poverty rate at 16.7% and its child poverty rate at 21.6%, placing it above Kentucky, Ohio, Pennsylvania, Virginia, and Maryland in both categories. These figures do not show that one child care policy causes poverty, but they help explain why child care, workforce participation, and small-business stability are especially important policy issues in West Virginia. Data source: U.S. Census Bureau, 2024 American Community Survey 1-year estimates, Table S1701.

For many families, child care is connected to work schedules, treatment appointments, school, transportation, family routines, and financial stability. In recovery-oriented communities, these supports matter. A disruption in child care can produce cascading instability, especially when the parent is already balancing employment, business ownership, treatment needs, parenting responsibilities, and financial pressure. Which when instability happens it can be a trigger among other things such as stress. As discussed in a prior blog, Understanding Internal Triggers in Addiction Recovery is very important.

This is especially important in West Virginia because the state already faces high levels of economic vulnerability. The 2024 American Community Survey estimated West Virginia’s overall poverty rate at 16.7%, compared with a national ACS poverty rate of 12.1% (U.S. Census Bureau, 2025). West Virginia’s poverty rate was reported as the fourth highest among the 50 states and the District of Columbia in 2024, and its child poverty rate was reported at 21.6%, the fifth highest in the country (West Virginia Center on Budget and Policy, 2025). In practical terms, that means more than one in five West Virginia children were living in poverty in 2024. These numbers do not prove that any single child care rule causes poverty, but they do show that child care policy operates in a state where many families are already financially strained.

That context matters when evaluating policies that affect working parents. Child care assistance is not only a family-support program; it is also connected to workforce participation, income stability, and the ability to keep predictable routines. If a parent loses child care, the effects may extend beyond one missed workday. It may affect the parent’s ability to maintain customers, complete jobs, attend treatment appointments, keep transportation reliable, pay employees, or continue building a small business.

For people in addiction recovery, instability can also become clinically relevant. Stress is widely recognized as a relapse risk factor, and research has described stress as a significant contributor to addiction vulnerability and relapse risk (Sinha, 2008). This does not mean financial stress automatically causes relapse, and it should not be framed that way. However, recovery often depends on structure, routine, social support, employment stability, and reduced exposure to avoidable stressors. When child care instability threatens work, income, parenting routines, and treatment access at the same time, it can create the type of pressure that recovery-oriented systems should try to reduce.

This also connects to the pride and stability that can come from building a legitimate small business. For some parents in recovery, forming an LLC may represent more than a legal structure. It may reflect accountability, business banking, liability protection, professional credibility, insurance needs, customer contracts, and a concrete step toward long-term self-sufficiency. A policy that discourages or penalizes that formal structure may unintentionally work against the same stability that recovery, workforce participation, and economic-development efforts are trying to support.

A balanced child care policy can still require verification. Income, household size, work activity, business records, need for care, and program-integrity rules all remain important. The concern is whether LLC ownership alone should interrupt support when the parent remains low income, is actively working, and can document legitimate self-employment. In a state with high poverty, high child poverty, and ongoing workforce challenges, child care policy should be reviewed through the lens of family stability, recovery support, and economic mobility.

What a Modernized Framework Could Look Like

Verification Without Automatic Exclusion

A modernized framework would not remove verification. It would only strengthen it. Applicants could be required to document income, business activity, hours, invoices, tax filings, contracts, receipts, business expenses, and need for care. Agencies could still deny applicants who fail to document qualifying activity or who exceed income limits.

The important difference is that the business structure itself would not end the analysis. A single-member LLC owner could be evaluated through the same practical questions used for other self-employed applicants: Is the parent working? Is the income countable and within limits? Is child care needed? Are records sufficient?

Better Alignment With Economic Development

This approach would align child care policy with entrepreneurship and economic-development goals. It would encourage formal business records, tax compliance, insurance, business banking, and legitimate documentation. It would also reduce the risk that parents feel pressured to dissolve or avoid an LLC simply to maintain child care support.

Why Reporters and Policymakers Should Care

The Story Is Larger Than One Family

The issue may begin with one family or one small business, but the policy question is broader. If a rule affects self-employed parents across the state, it may influence workforce participation, child care providers, small-business development, and family stability. That makes it a legitimate public-policy topic. And from impact surveys we have completed, this is true, and the effects of this policy are having negative impacts across the state.

Questions Worth Asking

Reporters and policymakers may want to ask:

How many families have been affected by the business-structure rule?

How many child care certificates involve self-employment?

Were families previously approved under older interpretations? (spoiler, the answer is YES)

How are caseworkers trained to apply the LLC exclusion?

What would it cost or require evaluating LLC owners through income and documentation instead?

How do neighboring states preserve program integrity without the same categorical exclusion?

Would policy change help benefit the residents of West Virginia?

These questions are fair because they focus on administration, consistency, outcomes, and comparison rather than personal blame.

Conclusion

West Virginia’s reviewed child care subsidy framework is more restrictive and more entity-structure focused than neighboring states reviewed. Pennsylvania, Kentucky, Virginia, Maryland, and Ohio generally appear to evaluate self-employment through income, work activity, and documentation. Pennsylvania, Kentucky, and Virginia provide especially strong comparisons showing that LLCs or formal business structures can be evaluated without automatic exclusion.

The question is not whether West Virginia should eliminate verification. It should not. The question is whether West Virginia can protect program integrity while recognizing legitimate self-employment through modern business structures. For a state facing workforce, economic, recovery, and family-stability challenges, that question deserves serious attention. And on the recovery aspect, West Virginia is finally seeing decreases in the effects of the opioid epidemic, which this new policy change could have negative consequences on. Read the blog on Opioid Epidemic in West Virginia – A Hope for Recovery to learn how there is hope to an end to this epidemic.

References

Federal Reserve Bank of St. Louis. (2026). May 2026 release tables: Labor force participation rate. FRED. Data from U.S. Bureau of Labor Statistics. https://fred.stlouisfed.org/release/tables?eid=784070&rid=446

Gurrentz, B. (2021, October 12). Child care subsidies help married moms continue working, bring greater pay equity. U.S. Census Bureau. https://www.census.gov/library/stories/2021/10/measuring-impact-of-child-care-subsidies-on-working-moms.html

Internal Revenue Service. (2025). Single member limited liability companies. https://www.irs.gov/businesses/small-businesses-self-employed/single-member-limited-liability-companies

Kentucky Cabinet for Health and Family Services. (2026). Volume VIII: Child Care Assistance Program policy manual. https://www.chfs.ky.gov/agencies/dcbs/dfs/Documents/omvolviii.pdf

Maryland State Department of Education. (n.d.-a). Child Care Scholarship Program. https://earlychildhood.marylandpublicschools.org/child-care-providers/child-care-scholarship-program

Maryland State Department of Education. (n.d.-b). Self-employment attestation statement. https://earlychildhood.marylandpublicschools.org/system/files/filedepot/2/self-employment_attestation_statement.pdf

Morrissey, T. W. (2017). Child care and parent labor force participation: A review of the research literature. Review of Economics of the Household, 15(1), 1–24. https://doi.org/10.1007/s11150-016-9331-3

Pennsylvania Department of Human Services. (n.d.). Child Care Works (CCW): Subsidized Child Care Program. https://www.pa.gov/agencies/dhs/resources/early-learning-child-care/child-care-works

U.S. Census Bureau. (2025). Poverty status in the past 12 months (Table S1701). 2024 American Community Survey 1-year estimates subject tables. https://data.census.gov/table/ACSST1Y2024.S1701

U.S. Department of Health and Human Services, Administration for Children and Families, Office of Child Care. (2025). Office of Child Care fact sheet. https://acf.gov/occ/fact-sheet

U.S. Small Business Administration. (2025). Choose a business structure. https://www.sba.gov/business-guide/launch-your-business/choose-business-structure

U.S. Small Business Administration, Office of Advocacy. (2025). 2025 small business profile: West Virginia. https://advocacy.sba.gov/wp-content/uploads/2025/06/West_Virginia_2025-State-Profile.pdf

U.S. Small Business Administration, Office of Advocacy. (2025, June 30). New Advocacy report shows the number of small businesses in the U.S. exceeds 36 million.

Virginia Department of Education. (2023). Child Care Subsidy Program guidance manual. https://ris.dls.virginia.gov/uploads/22VAC40/dibr/VDOE%20Child%20Care%20Program%20Guidance%20Manual%205.3.2023-20240822104447.pdf

West Virginia Department of Human Services. (2024). Child Care Subsidy Policy and Procedures Manual. https://dhhr.wv.gov/bcf/Childcare/Documents/WV%20Child%20Care%20Subsidy%20Policy%2010%201%202024.pdf

West Virginia One Stop Business Portal. (n.d.). Register your business.

West Virginia Secretary of State. (2026, March 10). Secretary of State Kris Warner reports 1,733 new WV business registrations for February 2026.